")

The recent merging of oil and gas companies in the U.S. indicate that energy majors see a long-term future for specific hydrocarbons in the energy transition. Chevron’s announcement of their US$53 billion all stock acquisition of Hess, and ExxonMobil’s US$59 billion merger with Pioneer Natural Resources, is likely the beginning of a wider industry consolidation in which oil majors target independent producers operating in relatively stable jurisdictions with proven light crude reserves, low breakeven costs, and flexible oil supply (i.e., shale wells that can start producing quickly when oil prices are high). Oil majors will continue to prioritize assets that generate significant free cash flows so they can continue paying large dividends to shareholders.

High cost of capital make greenfield assets hard to finance

Financing greenfield energy assets in emerging markets has become extremely challenging with the rise of interest rates. Hydrocarbon assets, which most investors are shying away from, and low carbon technologies, some of which do not yet have proven paths to profitability, are struggling to attract investments in developing markets as the risk-return is simply unjustifiable in the current financial environment. Outright acquisitions and mergers, however, have become more appealing, and none more so than the Stabroek Block in Guyana. The biggest discovery in the last decade has an estimated 11 billion barrels of recoverable oil equivalent, with potential to grow even more in the future. This is a multi-decade production play, and it signals Chevron’s commitment to a long-term hydrocarbon strategy in the Americas.

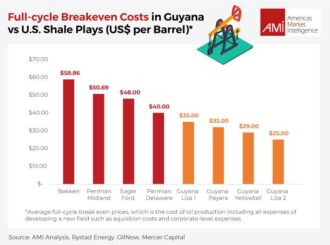

For years, Hess has known they’ve struck the jackpot with Guyana, reflected by the upbeat mood internally at the company. They’ve been seeking a large payday for quite some time—well deservedly so, as Guyana’s Stabroek Block has been praised as the best oil find in recent times. In addition to its resource potential, the ExxonMobil-operated block offers highly competitive breakeven costs ranging from $25 to $35 per barrel across producing projects. It is located offshore, where there tends to be less direct impact on communities than onshore drilling, and it also operates under a favorable production sharing agreement with attractive fiscal terms.

Image 1: Breakeven costs

Five major implications for Guyana

The Chevron-Hess deal will have five major implications for the Guyanese economy, all of which are likely to lead to long-term reverberations for the local oil and gas sector:

- An accelerated exploration of the Stabroek block

- ExxonMobil’s $63 billion dollars in free cash flow in 2022 makes it one of the most well-capitalized oil and gas companies in the world. The speed of their ramp up in Guyana has been unprecedented, both in terms of time to market and successfully drilled wells. However, with another oil major joining the Stabroek consortium, it is likely that the 10 to 12 wells planned for 2024, and the 35-well exploration campaign announced through 2028, will actually exceed the original numbers.

- An increase in production estimates for existing wells

- While the Stabroek consortium already has one of the most, if not the most, competent, and technical team in the oil and gas industry with ExxonMobil at the helm, there are technological advances that Chevron could bring to the table that could increase production estimates for Guyana (upwards from the 1.2mn projected for 2027). Chevron CEO Mike Wirth discussed their collaboration with AI juggernaut OpenAI noting “We’ve been working with OpenAI for multiple years now on technologies that could work in our industry,” Wirth said. He noted oil giants generate immense datasets on geological characteristics and more. Often times, these innovative technologies are siloed inside companies, with Chevron already suggesting that they will introduce new technical capabilities to the Bakken assets owned by Hess.

Image 2: Oil production

- A more competitive oil and gas sector

- Although Exxon will still be calling the shots as the lead operator of the Stabroek consortium, the presence of another American oil major will lead to more collaborative decision making behind closed doors. Chevron will also now be part of the bid made in the recent oil tender by Exxon, Hess and CNOOC, pacifying some of the government’s claims that ExxonMobil is the only game in town.

- Greater Chinese influence outside of the oil & gas sector

- Although the third partner in the Stabroek consortium is Chinese (CNOOC), the state-owned oil company has remained in the background during the last eight years of oil development in Guyana. Now, with the presence of two of the largest American oil majors in the consortium, CNOOC’s influence is likely to diminish. In turn, the Chinese government will increase its presence in surrounding sectors such as mining, healthcare, renewable power, and road infrastructure.

- Greater pressure from the government and the people

- With more resources, comes greater responsibility. The Guyanese government will likely highlight this acquisition to show that interest in Guyana remains hot, using the momentum to sign production sharing agreements that are less beneficial for oil companies in the most recent oil auction. The Guyanese people will also be more inclined to see what they can get out of a new major company coming into the country, both in terms of jobs and greater concessions. Despite the Wall Street Journal recently reporting that Guyana is booming, the reporting also raised questions on how the material improvement is flowing to ordinary Guyanese. It is expected that there will be more public pressure for improved living conditions in Guyana.

Chevron is bullet-proofing their portfolio against international turmoil

Although Hess’ 30% participation in the Stabroek consortium was the main reason behind Chevron’s acquisition, Hess also produces 190,000 barrels per day in the Bakken Shale Play where it owns 465,000 acres of land. The Bakken formation is both more mature and smaller than the Permian basin, signaling less room for growth, but the abundance of land means Chevron could drill new wells in new locations as old wells mature.[1] This flexibility, during a time of geopolitical turmoil, is exactly what Chevron is looking for as it seeks to bullet-proof its portfolio against unstable regimes and international conflicts.

Chevron also announced that the Bakken asset will provide a constant level of production, and strong cash flows, for many years to come. In fact, if the number of rigs remain constant, at four, Chevron estimates that the Bakken acquisition will have at least 15 years of inventory.[2] Although the Bakken has high half-cycle breakeven costs, at U$58 per barrel, Chevron’s resources means that it faces less pressure to stick to modest production increases like many other shale producers.[3] Its deep pockets, and ability to keep providing returns to shareholders, means that Chevron can afford to take riskier bets. [4]

Arthur Deakin is the Director of the Energy Practice at AMI (Americas Market Intelligence). Through market research and strategic analysis, he helps companies expand into Guyana and the wider Latin American region. In the past ten years, AMI has helped companies understand the Guyanese market, navigate Guyana’s local content legislation, execute pre- and post-acquisition due diligence and conduct competitive analysis on key players in the country.

[1] October 2023, Reuters, “Chevron-Hess deal may lift Bakken oil output, but no return to boom days.”

[2] October 2023, Chevron Press Release, “Chevron Announces Agreement to Acquire Hess Edited Transcript.”

[3] Rystad Energy

[4] October 2023, Reuters, “Chevron-Hess deal may lift Bakken oil output, but no return to boom days.”

{kind=link}